The last decade was first characterised by a series of breakthroughs in the development of optical device building blocks using silicon photonics followed by a spate of silicon photonics, start-up acquisitions. More recently, silicon photonics has entered a quiet period. But in May, Acacia Communications, a maker of coherent optical modules and a silicon photonics specialist, made headlines by raising $103.5 million in a successful initial public offering (IPO).

The IPO meets Mario Paniccia’s definition of the tipping point for silicon photonics. Paniccia, who was at Intel for 20 years and headed its silicon photonics development programme until 2015, defines the tipping point as when people start believing a technology is viable and are willing to invest.

He cites the American Institute for Manufacturing Integrated Photonics (AIM Photonics) venture, the $610 million public and private funded initiative set up last year to advance silicon photonics-based manufacturing. Other examples include the silicon photonics prototyping service coordinated by nanoelectronics research institute imec in Belgium, and the photonics capabilities developed by global chip-maker STMicroelectronics.

‘All these are places where people not only see silicon photonics as viable, but are investing significant funds to commercialise the technology,’ said Paniccia. ‘There are numerous companies now selling commercialised silicon photonics, so I think the tipping point has passed.’

Graham Reed, professor of silicon photonics at the University of Southampton’s Optoelectronics Research Centre, offers an academic perspective. In the 1990s it was more difficult to get funding to research silicon photonics, he says. Now, his group is regularly approached by companies from all over the world, which are either active in silicon photonics or plan to enter the market.

Status update

Optical integration has long been viewed as a promising tool to enable the industry to keep pace with the demanding requirements driving the datacom and telecom markets. In both markets, data traffic continues to grow, requiring system designers to develop denser transport and switching platforms, while keeping their cost and power consumption under control.

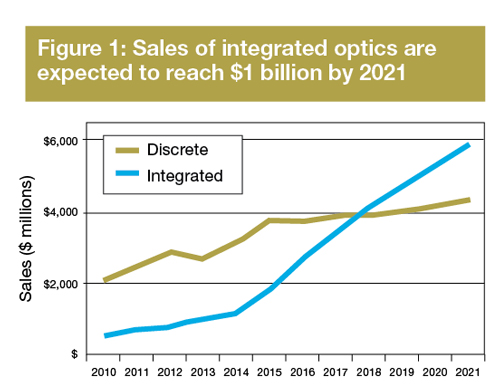

Yet a recent report on optical integration by market research firm LightCounting highlights how only one in 40 optical components sold to the datacom and telecom markets is an integrated device, even though such components generate a third of the global optical component market’s revenues.

‘Contrary to the expectation that integration is helping to reduce the cost of components, it is only being used for very high-end products,’ explained Vladimir Kozlov, CEO of LightCounting.

An extreme example is optical transport systems developer Infinera, which recently launched its latest generation photonic integrated circuit (PIC) design based on indium phosphide. The optical engine comprises a pair of PICs integrating hundreds of individual functions, which can deliver up to 2.4Tb/s of DWDM capacity. This represents a near-fivefold increase in capacity compared to Infinera’s existing 500Gb/s product, launched in 2011.

LightCounting’s report forecasts the total market for integrated devices through to 2021 and assesses the market opportunities for silicon photonics. The report concludes that the market impact of silicon photonics will not be significant in the next five years, although it will grow threefold to become a $1 billion market by 2021. By then, one in 10 optical components will be integrated, and integrated devices will account for 60 per cent of global revenues for optical components. Sales of integrated indium phosphide and gallium arsenide products, including products based on laser arrays and electro-absorption modulated lasers (EMLs), are projected to reach $5 billion in the same time frame.

Although silicon photonics has only recently become a viable technology for optical integration, its progress over the last few years has been striking. In just over a decade, the industry has gone from not knowing whether silicon could be used to make basic optical functions, such as modulators and photodetectors, to getting them to work at speeds in excess of 40Gb/s.

‘I’d argue the performance [of silicon photonics] is close to what you can get in III-V [materials such as indium phosphide and gallium arsenide],’ said Paniccia, who was directly involved in Intel’s key silicon photonics device breakthroughs.

Chris Doerr, who was at Bell Labs for more than 17 years, developed integrated optical devices first in indium phosphide and then also using planar lightwave circuits. He became hooked on silicon photonics after designing his first chip, an integrated coherent receiver, in 2009.

When fabricating a complex design using indium phosphide, five or six devices would need to be tested before a working one was found, he recalled. ‘In silicon it totally changed,’ he said. ‘The yield is so high that you could assume every device was good.’ It means you can focus more on the design than the yield aspects, says Doerr, now associate vice president of integrated photonics at Acacia Communications, having joined the company in 2011.

Another benefit Doerr highlights is that the optical performance of a silicon photonics chip closely matches its simulation results. ‘Using indium phosphide, you have to worry about all the composition effects, and the etching is not as precise. With silicon photonics, you know the dimensions and the refractive indexes and you can simulate and design very accurately.’

The result is that companies are no longer investing their time and effort to develop basic devices in silicon photonics, but are able to develop and sell a range of integrated subsystems.

LightCounting, which tracks optical component and module shipments, highlights several silicon photonics products now shipping in volume such as Cisco’s CPAK optical transceivers, while silicon photonics start-up Luxtera has long been shipping its 40Gb/s PSM4 modules, a market that it leads. LightCounting also forecasts that at least 100,000 100Gb/s PSM4 modules will ship this year, with more than half of them silicon-photonics based.

STMicroelectronics, meanwhile, is already sampling its 100G optical engine chip design for PSM4 modules, its first silicon photonics product. ‘Silicon photonics as a market is at a turning point this year,’ claimed Flavio Benetti, group vice president, general manager digital and mixed processes ASIC division at STMicroelectronics.

At the OFC show in March, Acacia announced that since September 2014 it had shipped 13,000 of its AC100 100Gb/s coherent CFP transceivers based on its silicon photonics PIC. The company also announced that it has started sampling optical modules based on the CFP2-ACO Implementation Agreement defined by the Optical Internetworking Forum (OIF).

Challenges

Despite the recent successes, silicon photonics technology continues to contend with a number of challenges that will take time to resolve.

The most significant one remains the laser source. Silicon alone cannot generate light, requiring that a laser source in another material is integrated onto the chip. Companies have developed several approaches to integrate the light source but a winning approach has yet to emerge.

Until a low-cost approach emerges, silicon photonics will not be able to compete with existing low-cost light sources such as vertical-cavity surface-emitting lasers (VCSELs), says Acacia’s Christopher Doerr. VCSELs dominate short-reach links, typically up to one hundred metres, although extended-reach VCSEL designs of several hundred metres also exist.

Equally, coupling the laser to a fibre or the silicon chip’s waveguide using passive alignment is another challenge. ‘Everything about silicon photonics is about low cost,’ said Southampton University’s Graham Reed. At present, to attach a laser, it is typically turned on and aligned to the chip’s waveguide. This requires manual intervention and is time-consuming.

‘The ideal scenario is to put a fibre down and it couples to the waveguide or laser and somehow you have aligned it,’ he explained. The challenge is the discrepancy in dimensions between the 10-micron fibre core and the waveguide, which is typically between 0.35 and 0.5 microns wide. Work is on-going to use mode converters or gratings such that the resulting optical loss is low enough to make passive alignment viable.

‘People still view it [the laser attachment] as a traditional optics assembly,’ said Doerr. ‘Until we get out of that mind-set and get to an electronics-type packaging where we can attach the fibre passively, we can’t truly break out of the cost structure of today’s optics.’ However, he is confident that passive alignment is coming.

Wafer-scale testing remains another challenge. Grating couplers are one way that designs can be tested while still on the silicon wafer. These allow the whole circuit to be tested, but not individual components: either it works or it doesn’t. ‘If you are going to mimic the successes of electronics, you need to test more comprehensibly than that,’ said Reed.

His group has developed an erasable grating that can be placed either side of an individual component to test it. These gratings can then be removed from the final circuit using laser annealing.

Another issue is the emergence of silicon photonics foundries. Chip volumes in silicon photonics manufacturing are several orders of magnitude lower than those in electronics. ‘This keeps the top foundries from diving in and, until that happens, you won’t see the cost reductions and volume increases people are hoping for,’ said Doerr.

Opportunities

The industry’s resolve to overcome these challenges will only benefit from the growing market opportunities for silicon photonics.

One market driver is the growing demand of the large-scale data centre players, such as Microsoft, for higher-speed interfaces. ‘Their appetite increases as the industry is making progress,’ said Kozlov. ‘Six months ago they were happy with 100 gigabit; now they are really focused on 400 gigabit.’

Going to 400Gb/s interfaces will require four-level pulse-amplitude modulation (PAM-4) transmitters, sparking new competition between indium phosphide, VCSELs and silicon photonics, he says.

Silicon photonics may even have an edge according to results from Cisco, which show that its silicon photonics-based modulators work well with PAM-4 designs. Silicon photonics could even take the market lead here, says Kozlov, for 400-gigabit designs that require multiple PAM-4 transmitters on a single chip.

Another promise of silicon photonics – although still to be demonstrated – is the combination of optics and electronics in one package. Such next-generation 3D packaging, if successful, could change things more dramatically than LightCounting currently anticipates, according to Kozlov.

STMicroelectronics is using 3D packaging to create its 4x25Gb/s PSM4 transceiver design using two chips. The optical engine, implemented in silicon photonics, integrates four modulators, four detectors and the grating couplers used to interface to the fibre. The second device, a 55nm BiCMOS chip, houses the transceiver’s associated electronics.

‘The 3D packaging consists of two dies, one copper-pillar bonded to the other,’ said Benetti. ‘It is a dramatic simplification of the mounting process of an optical module.’

However, Andrew Rickman, CEO and founder of UK start-up Rockley Photonics, believes silicon photonics cannot achieve its full potential by going after the market for 100G and 400G interconnects for the data centre. Instead, Rickman believes silicon photonics should be viewed as one element – albeit an important one – in an array of technologies used to tackle system-level issues.

‘If you take control of enough of the system problem, and you are not dictated to in terms of what Multi-source agreement [MSA] or what standard that component must fit into, and you are not competing in this brutal transceiver market, then that is when you can optimise the utilisation of silicon photonics,’ said Rickman. ‘And that is what we are doing.’

Rockley has yet to launch its product, but has said it is designing a silicon photonics switch chip along with a controller ASIC and interconnect protocol to tackle a core problem in mega data centres – how to connect more and more servers in a cost-effective and scalable way.

The start-up is a fabless chip company and will not be building systems. Instead, Rockley will supply its chipset-based reference design, its architecture IP and software stack to its customers to create custom line cards and fabric cards. The resulting system is designed as a drop-in replacement for the large-scale data centre players’ switches they already deploy, yet will be cheaper, more compact and consume less power, according to Rickman.

Acacia can be viewed as another player taking control of the coherent transmission system in that it develops its own low-power coherent digital signal processor ASIC as well as the coherent transceiver PIC. Acacia may not be competing in the fiercely competitive intra-data centre market, but it is up against optical module players developing CFP2-ACO analogue coherent optical modules using indium phosphide.

Doerr believes the opportunities for silicon photonics will improve as more and more channels are integrated on a device, and with closer integration with the electronics – either co-packaged or using a 3D stack.

For coherent designs, Doerr expects to see further reductions in the size, cost and power consumption using silicon photonics, making it competitive with other optical transceiver technologies for distances as short as 2km.

‘You can use high order modulation formats such as 256-QAM and achieve very high spectral efficiency,’ said Doerr. Using such a modulation scheme would require fewer overall lasers to achieve significant transport capacities, improving the cost-per-bit performance for applications such as data centre interconnect.

Disruptive technology

Will silicon photonics displace other technologies? That’s the billion-dollar question in the industry right now. But views are mixed as to whether silicon photonics is genuinely disruptive.

‘If you look at the origins of what a disruptive technology is, it is a technology that works in one field that but then it performs so well, it crosses the boundary into other areas,’ said Reed. Silicon photonics was initially regarded as a short-reach technology, but once the performance of its modulators started to increase drastically, the technology crossed the boundary into long-haul research, he notes. ‘That is the definition of a disruptive technology,’ he observed.

Rickman also believes silicon photonics is disruptive: ‘It is a paradigm shift; it is not a linear improvement.’ But he argues it has to have the right features and be used in the right way when addressing systems design.

Instead of viewing silicon photonics as a ‘Band-Aid’ for semiconductors to delay the ending of Moore’s law, the key is to know the capabilities of silicon photonics and electronic ICs, and to organise them in a way that overcomes the ‘exhaustion of Moore’s law and the input/output problems’, he says.

Acacia’s Christopher Doerr agrees. ‘I don’t think we have hit the limitation at all,’ he said. ‘As we integrate more channels, being disruptive will be undeniable.’

Others do not view silicon photonics as disruptive, however. ‘The theory of disruption is that new technologies always come from the low end, and then end up dominating the market,’ said Kozlov, ‘whereas silicon photonics, like optical integration more generally, is entering the market at the high-end.’

But Kozlov acknowledges that the technology has performance disadvantages, compared to traditional technologies such as indium phosphide and gallium arsenide, and its optical performance is continually improving. ‘That may still be consistent with the theory of technological disruption,’ he noted.

‘I don’t know about disruptive; it is a word that is used too much,’ commented Mario Paniccia. Silicon photonics is a technology that opens up a lot of new possibilities, as well as a new cost structure and the ability to produce components in volume. But it doesn’t solve every problem, he says.

Optical players very much focus on cost. For markets such as the large-scale data centre, it is all about achieving the required performance at the right cost. Paniccia thus expects silicon photonics, indium phosphide and VCSELs all to co-exist. ‘It is all about practical decisions based on price, performance and good-enough solutions,’ he concluded. l

- Roy Rubenstein is a freelance science writer based in Israel, and author of Gazettabyte.com